Rupee cost averaging is a popular investment strategy that usually gets even more popular in environments like this, where the markets are at all-time market highs but it has people worried that the next big stock market crash could be just around the corner be it because of high valuations or the pandemic or just profit booking.

And while rupee cost averaging can absolutely be a good way to ease yourself into the market, it’s a strategy whose pros and cons need to be understood clearly.

Rupee cost averaging is the practice of investing your money at regular intervals say monthly and mostly for a fixed amount instead of all at once.

Let’s say that you just received your bonus from your organisation and you have Rs 10,00,000/- that you’d like to invest for the long term. You could invest it all right away, or you average it out by investing, say, Rs. 1,00,000 per month over next 10 months.

The idea behind doing rupee cost averaging is :

To be clear, this is not the same as making a consistent contribution each month or every time you receive your salary. That’s a good practice, but it’s technically not rupee cost averaging because in that you are actually investing all of the money you have available to save as soon as it’s available.

Rupee cost averaging is really for situations like receiving a bonus or inheritance, or wanting to move money from a savings account to an investment account. Rather than investing some of your income as you receive it, these situations give you an unexpected sum of money that you have to decide what to do with.

The main benefit of Rupee cost averaging is that it reduces your investment risk. By keeping some of your money out of the market for some period of time, your overall investment strategy is temporarily more conservative and less susceptible to a market crash.

Risk reduction helps in making easier to invest emotionally and since investing is such an important part of building long-term wealth, it surely helps.

Supporters of rupee cost averaging argue that it can actually increase your returns. Because you contribute a pre-defined amount of money at pre-defined intervals, you will automatically buy more share/MF units when the stock market is down and fewer when the market is up. Better bang for your buck !

This is partially true. Rupee cost averaging does cause you to buy more shares/MF units when the market is down, and it can lead to better returns in a declining market. But as you’ll read further, this isn’t always the expected outcome.

While rupee cost averaging does reduce your investment risk, there are a few downsides to consider.

Almost every investment decision involves a decision on risk vs. returns. Higher risk means a possibility of higher returns and its true for other way round as well.

This hold true for rupee cost averaging. Although it can lead to better returns in some cases, most of the time the reduced risk comes with reduced returns.

The reason is simply that the stock market goes up more often than it goes down. So by investing your money in little bits over time instead of investing it all at once, your odds of missing out on gains are greater than your odds of avoiding losses. According to a 2012 Vanguard study, investing all of your money at once would historically have produced better returns than rupee cost averaging about 66% of the time. This might backfire when we are pretty sure that market Is headed for correction in short term but is that predictable ?

Nothing is guaranteed, but the fact is that you will get lower returns in exchange for lesser risk.

One of the biggest pieces of your investment plan is your asset allocation (refer to my earlier blog on this — Invest Right) Your asset allocation is the only way you can manage your expected risk and return, and you should choose your asset allocation knowing that one may lose money when markets are down. But how much are you willing to lose and for what period? The more fearful you are for losing your money, the more conservative your asset allocation should be.

Whatever you decide, rupee cost averaging by definition causes you to stray from that asset allocation plan. By temporarily keeping some of your money in cash, you are temporarily investing in a portfolio that is more conservative than you originally decided was appropriate based on your risk appetite.

So if you don’t feel comfortable investing your money all at once, then probably your asset allocation strategy is more aggressive than what it should be. The solution may simply be to invest your money all at once into an asset allocation that’s more conservative, and therefore less vulnerable to loss in case of a market crash.

Finally, rupee cost averaging can make your life more difficult. Setting up periodic contributions takes more work, time and monitoring rather than investing your money all at once.

A conservative asset allocation can probably be more beneficial and simpler to follow.

Let me take an example to explain the above points

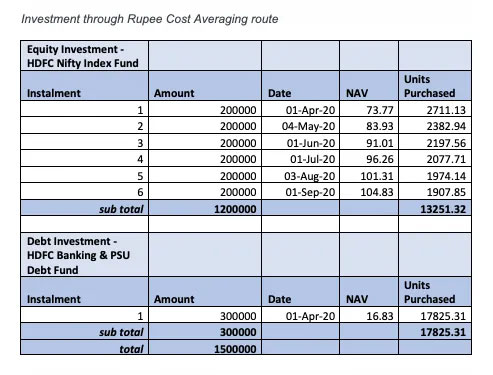

Suppose you get a bonus of Rs. 15,00,000 in March 2020 for your performance. Considering the pandemic situation at that time you decide not to go ahead with your asset allocation which normally is Aggressive (80% Equity and 20% Debt). Instead you decide to spread out your equity investments over a 6 month period and invest the 20% debt allocation immediately.

Here is what your returns on the investment be :

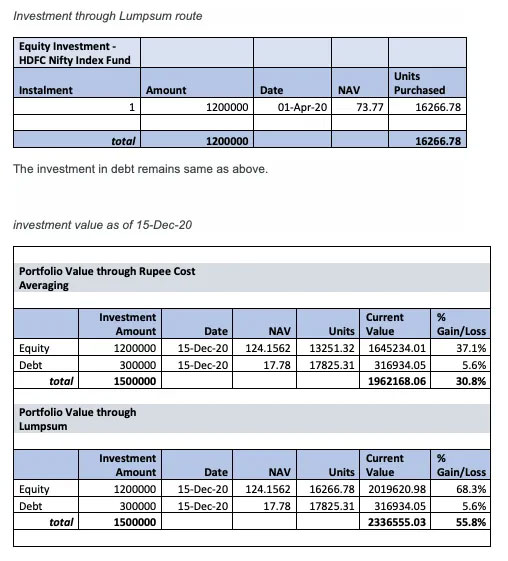

I am taking an example of a HDFC Nifty Index Fund for equity investment and HDFC Banking & PSU Debt Fund Debt Fund (note — no special bias for taking this fund so don’t take it as a recommendation from our side)

Investment through Rupee Cost Averaging route

A difference of 25% returns in absolute terms ! These last 8 months might be a one off incidence in stock markets but still shows the returns difference in the two strategies.

So with all this information, the question is: what strategy to follow — rupee cost averaging or all in ?

Here’s my take:

At the end what matters is — "time in the market and not timing the market”.

Happy Investing !